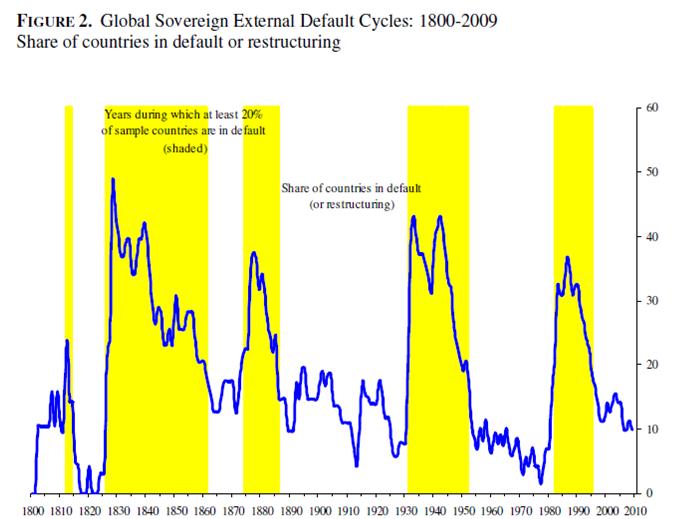

Carmen Reinhart and Kenneth Rogoff have written an especially relevant article in the latest issue of The American Economic Review titled "From Financial Crash to Debt Crisis." Many of the concepts are in their latest book, This Time is Different: Eight Centuries of Financial Folly. They create a new and more detailed data series concerning public debts in many countries, developing and developed over a two century period.

The article has four main points:

1) Debt to foreign creditors usually happens before a banking crisis

2) Bank crises precede or are simultaneous with sovereign debt crises

3) Public borrowing surges right before sovereign debt crises

4) Public and private borrowing frenzy with bursts of hyperinflation

They meticulously document this through long data series of public debt, which show cycles. These cycles are longer than a generation; they foster a "This time is different" approach to handling the situation (usually with more debt). The policy makers believe that they are smarter and have better systems of handling financial issues than previous episodes. The history shows that they are wrong about this.

These issues remind me of the old ideas of Nikolai Kondratieff. He first observed large historical waves within the economy that tended to last 40 to 60 years. He noticed several stages within the waves.

The first stage is economic expansion. These expansions often involved new technology, minor wars and social upheaval. The net effect is a large amount of new investment. The second stage is the peak. General affluence causes shortages and production becomes strained to keep up. This stage is also marked by a different type of war, that of absolute wars. The first adjustment typically happens at the end of the absolute war. The public debt grows so large that the economy must adjust for more balanced budgets.

The stage that he describes as the plateau is actually the initial phase of the decline. It is actually a slight decline, that is marked by an increase in speculation. The next phase is the panic. This is marked by bank failures and sharp declines in public confidence. The next stage is the decline, and it is marked by a lack of confidence and doubt.

Kondratieff was never able to fully explain why these happened with such regularity other than with data. Another issue was that he was not able to explain their variation in amount of years. Because of this, and the fact that he was murdered in one of Joseph Stalin's purges, his ideas have not been well accepted in the world of economics. These ideas were popularized in the western world by Joseph Schumpeter, in his book, Business Cycles, "incessantly destroying the old one, incessantly creating a new one. The process of Creative Destruction is the essential fact about capitalism."

One of the standing observations in long wave literature is that wars are an essential element to them. I would submit that wars could be turned into a more general government expense and more importantly debt. Far and away, the most common way that government's went into debt was through war until the last century. Now, there are several main ways that governments have acquired large debts in the past wave. War has certainly still been a feature, but social welfare has become an increasingly public function in the past 100 years. Wealth transfers and subsidized loans from developed to developing countries has continued even after colonialism has largely subsided. Bureaucracy, in some countries such as the United States, has become larger in the past 100 years. The culmination of these factors has created increases in government expenditure. So while we may have escaped a peak without an all out war, we have more than made up for it with other government expenditures and most critically, debt.

Now, as we are in a panic, and we are potentially observing defaults and bankruptcies. Confidence is certainly becoming lower and lower, I think these ideas are worth revisiting. The reason that I tie Reinhardt and Rogoff's works to Kondratieff and Schumpeter is that I think Reinhardt and Rogoff may actually be observing critical factors of peaks, panics, and the decline... while ignoring the larger picture. Rogoff, in recent interviews, has spoken about public debt overhangs crippling economies for long periods of time. These debt overhangs probably are the result of government expansion, which led to periods of increased monetary base, only to be met with malinvestment and over expansion. Keynesian economics would teach us to fight these panics and decline with further debt to return us to the production possibility frontier, but that only ends up adding to the debt overhang.

Of course, I have proved nothing and this will need much more study. I think these issues relate to the heart of our current financial crisis in Europe and by contagion the rest of the world. The question 'should we bail out our banks' is never a pleasant one, but the amount of debt that the nation takes on likely has much to do with the length of its decline. Kondratieff explained the decline as a period that lacked confidence, but it lacked confidence because of fearful business conditions. Perhaps Rogoff's "debt overhang" plays a part in that.

Works Consulted:

Goldstein, Joshua. Long Cycles. New Haven: Yale University Press. 1988. Print.

Mager, Nathan. The Kondratieff Waves. New York: Praeger. 1987. Print.

Reinhardt, Carmen and Kenneth Rogoff. "From Financial Crash to Debt Crisis." The America Economic Review.

Pittsburgh: American Economic Association. August 2011. Journal.

Schumpeter, Joseph. Business Cycles. New York: McGraw-Hill. 1939. Print.

The article has four main points:

1) Debt to foreign creditors usually happens before a banking crisis

2) Bank crises precede or are simultaneous with sovereign debt crises

3) Public borrowing surges right before sovereign debt crises

4) Public and private borrowing frenzy with bursts of hyperinflation

They meticulously document this through long data series of public debt, which show cycles. These cycles are longer than a generation; they foster a "This time is different" approach to handling the situation (usually with more debt). The policy makers believe that they are smarter and have better systems of handling financial issues than previous episodes. The history shows that they are wrong about this.

These issues remind me of the old ideas of Nikolai Kondratieff. He first observed large historical waves within the economy that tended to last 40 to 60 years. He noticed several stages within the waves.

|

| Nikolai Kondratieff |

The first stage is economic expansion. These expansions often involved new technology, minor wars and social upheaval. The net effect is a large amount of new investment. The second stage is the peak. General affluence causes shortages and production becomes strained to keep up. This stage is also marked by a different type of war, that of absolute wars. The first adjustment typically happens at the end of the absolute war. The public debt grows so large that the economy must adjust for more balanced budgets.

The stage that he describes as the plateau is actually the initial phase of the decline. It is actually a slight decline, that is marked by an increase in speculation. The next phase is the panic. This is marked by bank failures and sharp declines in public confidence. The next stage is the decline, and it is marked by a lack of confidence and doubt.

|

| (source: http://www.longwavegroup.com/) |

Kondratieff was never able to fully explain why these happened with such regularity other than with data. Another issue was that he was not able to explain their variation in amount of years. Because of this, and the fact that he was murdered in one of Joseph Stalin's purges, his ideas have not been well accepted in the world of economics. These ideas were popularized in the western world by Joseph Schumpeter, in his book, Business Cycles, "incessantly destroying the old one, incessantly creating a new one. The process of Creative Destruction is the essential fact about capitalism."

One of the standing observations in long wave literature is that wars are an essential element to them. I would submit that wars could be turned into a more general government expense and more importantly debt. Far and away, the most common way that government's went into debt was through war until the last century. Now, there are several main ways that governments have acquired large debts in the past wave. War has certainly still been a feature, but social welfare has become an increasingly public function in the past 100 years. Wealth transfers and subsidized loans from developed to developing countries has continued even after colonialism has largely subsided. Bureaucracy, in some countries such as the United States, has become larger in the past 100 years. The culmination of these factors has created increases in government expenditure. So while we may have escaped a peak without an all out war, we have more than made up for it with other government expenditures and most critically, debt.

Now, as we are in a panic, and we are potentially observing defaults and bankruptcies. Confidence is certainly becoming lower and lower, I think these ideas are worth revisiting. The reason that I tie Reinhardt and Rogoff's works to Kondratieff and Schumpeter is that I think Reinhardt and Rogoff may actually be observing critical factors of peaks, panics, and the decline... while ignoring the larger picture. Rogoff, in recent interviews, has spoken about public debt overhangs crippling economies for long periods of time. These debt overhangs probably are the result of government expansion, which led to periods of increased monetary base, only to be met with malinvestment and over expansion. Keynesian economics would teach us to fight these panics and decline with further debt to return us to the production possibility frontier, but that only ends up adding to the debt overhang.

|

| Kenneth Rogoff (Photo: World Economic Forum) |

Of course, I have proved nothing and this will need much more study. I think these issues relate to the heart of our current financial crisis in Europe and by contagion the rest of the world. The question 'should we bail out our banks' is never a pleasant one, but the amount of debt that the nation takes on likely has much to do with the length of its decline. Kondratieff explained the decline as a period that lacked confidence, but it lacked confidence because of fearful business conditions. Perhaps Rogoff's "debt overhang" plays a part in that.

Works Consulted:

Goldstein, Joshua. Long Cycles. New Haven: Yale University Press. 1988. Print.

Mager, Nathan. The Kondratieff Waves. New York: Praeger. 1987. Print.

Reinhardt, Carmen and Kenneth Rogoff. "From Financial Crash to Debt Crisis." The America Economic Review.

Pittsburgh: American Economic Association. August 2011. Journal.

Schumpeter, Joseph. Business Cycles. New York: McGraw-Hill. 1939. Print.

Radiohead - "Codex"

No comments:

Post a Comment